What if your insurance company rejects your claim simply because you waited forty-eight hours too long to document the moisture? For many Sydney homeowners, the fear of a “gradual damage” exclusion is just as stressful as the initial burst pipe. You deserve to feel secure in your own home, not buried under confusing “escape of liquid” definitions while mould begins to take root in your floorboards. Mastering the water damage repair insurance process is the only way to ensure your property and your health remain protected.

We agree that navigating policy fine print during a crisis is overwhelming. This guide simplifies the restoration journey by providing the expert clarity you need to secure claim approval and stop hidden mould. You will learn how to navigate the complexities of your policy and ensure total moisture removal using a systematic, evidence-based approach. We will break down the 2026 NSW regulatory changes affecting property owners, explain how to gather evidence that adjusters cannot ignore, and show you why professional moisture extraction is your best defense against long-term structural issues.

Key Takeaways

- Identify the critical difference between “sudden” and “gradual” damage to prevent insurers from rejecting your claim based on maintenance exclusions.

- Navigate the water damage repair insurance process with confidence by following a structured sequence of safety, mitigation, and professional evidence gathering.

- Compile an “unfiltered” evidence portfolio that adjusters cannot ignore, ensuring you receive the full replacement value for your damaged property.

- Protect your family’s health by using the Goldmorr System to eliminate airborne spores and moisture before secondary mould growth occurs.

What is the Water Damage Repair Insurance Process?

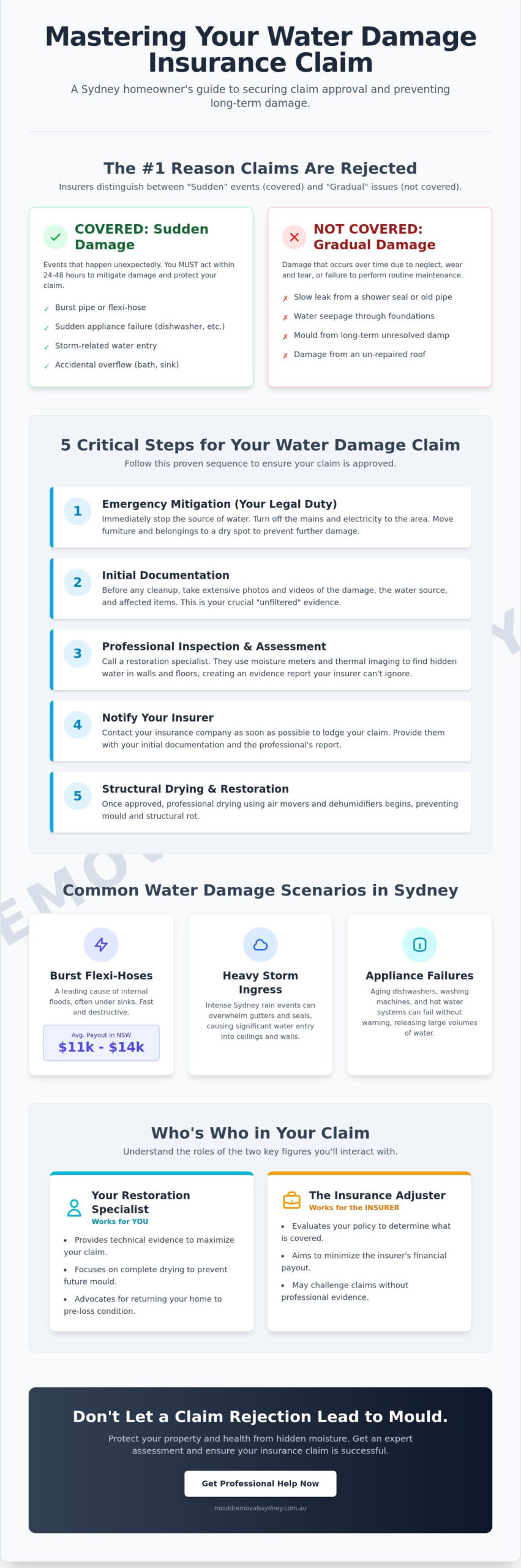

The water damage repair insurance process is a systematic sequence designed to return your property to a pre-loss state while securing financial reimbursement. It isn’t just about calling your provider; it’s a structured journey that begins with immediate mitigation, followed by professional assessment, and concludes with structural drying and restoration. In Sydney, the success of your claim hinges on demonstrating that the event was “sudden and accidental” rather than a result of long-term neglect or poor maintenance.

Water damage can compromise the structural integrity of your home within hours, making the distinction between “sudden” and “gradual” damage vital. Australian insurers generally cover sudden events like a pipe bursting overnight. They often reject gradual claims, such as a slow drip behind a shower wall that has existed for months. You must act within the first 24 to 48 hours to prevent secondary issues like mould. If you delay, your insurer might argue that the damage escalated because you failed to act, potentially leading to a claim rejection.

In the Sydney market, you’ll interact with two primary figures. The insurance adjuster works for the insurer to evaluate policy coverage and minimize the company’s financial exposure. Conversely, the restoration specialist works for you. They use moisture meters and thermal imaging to document the invisible spread of water. This data is essential for the water damage repair insurance process, as it provides the technical evidence required to justify a comprehensive payout. Without professional documentation, you risk leaving moisture behind, which leads to structural rot and health hazards.

Common Water Damage Scenarios in Sydney

Sydney homeowners frequently face internal plumbing failures. Burst flexi-hoses under kitchen sinks are a leading cause of claims in New South Wales, with average payouts for burst pipes often ranging between $11,000 and $14,000 according to industry data. Heavy storm ingress during intense Sydney rain events also contributes significantly to property damage. Additionally, aging appliances like dishwashers or washing machines often fail without warning, releasing hundreds of litres of water into cabinetry and subfloors.

The “Escape of Liquid” Clause Explained

An escape of liquid is the accidental and sudden release of water from a fixed system, such as a pipe or a water heater, within the property boundaries.

The term “fixed system” is vital for your claim success because it excludes portable items like buckets or movable garden hoses. If the water originates from a permanent fixture, your policy is more likely to trigger coverage. Insurers also distinguish between internal plumbing failures and external water entering from the ground up. Ground-up water is typically classified as “flood,” which often requires a specific policy rider that many Sydney homeowners may not realize they lack until the damage is already done.

5 Steps to Navigating Your Water Damage Claim

Success in your claim depends on speed and precision. The water damage repair insurance process follows a strict timeline where your actions in the first hour dictate the outcome of the next six months. You must transition from emergency response to professional documentation without missing a beat. This ensures your insurer has no reason to doubt the validity of your loss.

Step 1: Emergency Mitigation

Under Australian insurance law, you have a legal obligation to “mitigate loss.” This means you can’t simply leave a pool of water sitting on your floor while you wait for an adjuster to call you back. You must take reasonable steps to prevent further damage immediately. Turn off the water mains and, if it’s safe to do so, cut the electricity to the affected zones. Move timber furniture, rugs, and electronics to a dry area to prevent permanent staining or electrical hazards. When the situation is beyond your control, calling for emergency water damage repair is the most effective way to stabilize your property and satisfy your policy requirements.

Step 2: Initial Documentation. Before you start any major cleanup, capture the “unfiltered” state of the damage. Take high-resolution photos and videos of the standing water, the source of the leak, and any damaged belongings. Don’t throw anything away yet. Your insurer needs to see the extent of the loss in its original state to process your claim accurately.

Step 3: The Professional Inspection

A visual check is never enough. Water is invasive and often hides inside wall cavities or deep within subfloors. Our specialists use industrial-grade moisture meters and thermal imaging cameras to track exactly where the liquid has migrated. This data-driven approach is essential for insurance validity, as it provides an IICRC-standard assessment that adjusters can’t easily dismiss. Even if the surfaces feel dry to the touch, a professional mould inspection is vital for your long-term health. Spores can begin colonizing within 48 hours, and identifying these risks early is the only way to ensure your policy covers the necessary remediation.

Step 4: Claim Lodgement. Submit your restorer’s report and a detailed inventory list to your insurer. Use the technical data from our inspection to prove why specific drying equipment is required. This removes the guesswork for the insurance company and speeds up the approval process.

Step 5: Restoration and Monitoring. Once approved, the structural drying begins. We use high-velocity air movers and dehumidifiers to extract moisture from the air and building materials. We monitor these levels daily, only concluding the process when every material reaches its dry standard. If you need assistance documenting your loss correctly, our team can help you manage your water damage restoration and provide the evidence your insurer requires.

Covered vs. Not Covered: Addressing the #1 Claim Objection

Claim rejection is the primary fear for Sydney homeowners during the water damage repair insurance process. Most denials stem from the “gradual damage” trap. Insurers categorize any leak that has persisted over time as a maintenance failure. If an adjuster spots rust on a fitting or extensive rot in a subfloor, they may conclude the issue was preventable. Maintenance is your responsibility. You must prove the event was sudden to secure your payout.

Proving the Event Was Sudden

Professional moisture mapping provides a scientific timestamp by showing the precise saturation levels of building materials, which identifies the difference between a fresh burst and an old leak. We use this data alongside a licensed plumber’s report to verify a sudden mechanical failure. Sydney’s high humidity complicates this. Within just 72 hours, high moisture levels can cause building materials to warp or discolour. This makes a sudden event appear much older than it actually is. Our technical evidence prevents adjusters from misinterpreting these environmental effects and wrongly denying your claim.

You should also be aware of the “finding and fixing” rule found in most Australian policies. Insurers typically pay for the “access” required to find the leak and the “restoration” of the damage it caused. They do not usually cover the cost of the specific part that failed. If a pipe bursts behind a bathroom wall, the policy covers the demolition and drying of that wall, but you are responsible for the plumber’s bill to actually fix the pipe. Understanding this distinction helps you manage your budget and expectations from day one.

When Mould Becomes an Insurance Matter

Does your policy cover black mould remediation? Coverage only applies if the growth is “resultant damage” from a covered sudden event. If the growth is considered a “pre-existing condition” stemming from poor subfloor ventilation or a long-term leak, it will be excluded. The longer you wait to initiate the water damage repair insurance process, the higher the chance the insurer will claim the mould was preventable. We provide the documentation needed to prove the mould was a direct, immediate consequence of the water ingress rather than a result of neglect.

Waiting even a few days to report the damage increases the risk of “resultant damage” being excluded. Insurers argue that by delaying, you allowed the moisture to sit, which directly caused the mould to grow. This is why we prioritize fast, evidence-based mitigation. We ensure your claim is lodged with the proof necessary to show you did everything possible to protect the property.

Documentation and Evidence: How to Win Your Claim

Evidence is the primary currency of the water damage repair insurance process. Without clear, technical proof of the loss, your insurer may attempt to underpay or deny the claim based on a lack of clarity. You must act as a diligent historian of the event from the moment you discover the water. This requires more than just a few quick snapshots; it involves a comprehensive record of the damage, the source, and every subsequent interaction with your provider.

Start by creating a digital communication log. Record the date, time, and name of every person you speak to at the insurance company. Summarize what was promised or discussed in each call. This diary becomes invaluable if disputes arise later regarding timelines or coverage approvals. Pair this with high-resolution visual proof. Capture wide-angle shots to show the spread across rooms and close-up photos of specific points of failure, such as a split hose or a water-stained ceiling. If you notice swelling in skirting boards or discolouration on gyprock, document these details before the drying equipment changes their appearance.

The Anatomy of a Professional Restoration Report

While your photos are important, adjusters rely heavily on the technical Restorer’s Report to justify high-value payouts. This document provides a scientific snapshot of the property’s health. It includes moisture readings of structural materials like timber, gyprock, and concrete, comparing them against a “dry standard” from an unaffected area of the home. We also record atmospheric readings, specifically Relative Humidity and Grains Per Pound (GPP). These metrics prove the air is saturated enough to cause secondary damage, which justifies the use of industrial dehumidifiers and air movers. A professional scope of works then defines exactly what is needed to return your home to a pre-loss condition, leaving no room for the insurer to “guess” the repair costs.

Capturing Content Damage

One of the most common mistakes Sydney homeowners make is throwing away saturated items before the adjuster arrives. Never discard damaged belongings. Keep them in a “containment zone,” such as a garage or a tiled balcony, so the adjuster can verify the loss in person. For electronics, photograph the serial numbers and model labels clearly. This ensures you receive the correct replacement value for specific brands. For non-porous items like glass or metal furniture, we often utilize professional air purification and scrubbing to remove odours and spores, potentially saving family heirlooms that would otherwise be lost. If you are struggling to itemize your losses, our team can provide the technical water damage restoration documentation you need to secure a fair settlement.

Why ABC Mould Cleaning Solutions is Your Best Partner

Choosing the right specialist determines whether your property recovers fully or suffers from recurring mould issues. ABC Mould Cleaning Solutions provides specialised Water Damage Restoration that bridges the gap between emergency extraction and long-term safety. We understand that the water damage repair insurance process is often won or lost based on the quality of the initial intervention. Our team delivers the technical, insurance-ready reporting that adjusters rely on to approve your claim. We document every moisture reading and atmospheric change, ensuring your provider has a clear, undeniable record of the loss.

Our Sydney-wide expertise allows us to navigate the specific challenges of local architecture and climate. Whether you own a heritage terrace with complex subfloors or a modern high-rise apartment, we apply a systematic, evidence-based approach to your recovery. We use the Goldmorr System, our proprietary methodology, to eliminate airborne spores and surface contaminants during the drying phase. This professional-grade system offers a level of security that amateur or retail alternatives simply cannot match. We focus on pragmatic, results-driven solutions that return your home to a healthy state as quickly as possible.

Beyond Drying: Total Air Purification

Standard carpet drying fans are rarely sufficient in Sydney’s humid climate. High ambient moisture prevents effective evaporation, which often leads to the “musty smells” that indicate hidden water pockets and active bacterial growth. We go beyond simple drying by deploying industrial-grade Air Purification & Scrubbing units. These machines filter microscopic particles from your indoor environment while we use biodegradable fogging to neutralise odours at the source. This comprehensive approach ensures that once the structural materials are dry, the air your family breathes is clean and safe.

Your Next Steps to Resolution

Don’t let a sudden leak turn into a permanent health hazard or a rejected insurance claim. Take immediate action to stabilise your property and secure your financial rights. Contact our emergency response team to initiate a professional assessment. We will walk you through every stage of the water damage repair insurance process, from the first moisture map to the final clearance test. Our goal is to remove the anxiety of restoration by providing a clear, step-by-step path to a dry home. Book your inspection now to protect your insurance rights and ensure your property receives the expert care it deserves. We are ready to help you resolve this crisis today.

Secure Your Property and Your Payout Today

Mastering the water damage repair insurance process requires a combination of rapid response and meticulous evidence gathering. You now understand that documenting the “sudden” nature of the event is the only way to bypass common policy exclusions and secure your full entitlement. By acting within the first 48 hours, you stop moisture from becoming a permanent structural or health threat. Professional documentation ensures that adjusters see the full scope of the loss, leaving no room for underpayment or claim denial.

Don’t face the insurance adjusters alone. Our IICRC trained technicians provide the high-level technical reports and moisture mapping needed to validate your loss with certainty. We leverage the Goldmorr System to ensure your indoor air quality is restored to a safe, healthy standard. With our 24/7 emergency service available across all of Sydney, we are ready to stabilize your home the moment a crisis strikes. You don’t have to navigate the complexities of restoration and claims on your own; similarly, if you are seeking support for personal challenges, you can learn more about Sober Coach and their recovery programs.

Get Professional Help With Your Water Damage Claim Today

Your home is your most significant investment. Take the first step toward a successful recovery by securing the professional evidence your insurer requires. You can restore your property to its original condition and protect your family’s health with the right expert partner by your side.

Frequently Asked Questions

Does home insurance cover water damage from a leaking roof?

Yes, but only if the leak is caused by a sudden, accidental event like a severe Sydney storm or a fallen branch. Insurers typically exclude damage resulting from gradual wear and tear, rusted flashing, or poor maintenance. You must prove the ingress was immediate to succeed in the water damage repair insurance process. Professional documentation of the storm’s impact is often required to validate these claims.

How long do I have to file a water damage claim in NSW?

You should notify your insurer as soon as the damage is discovered to satisfy your duty of disclosure. While specific timeframes vary by policy, delaying the report can lead to claims of “gradual damage” or failed mitigation. Under the 2026 General Insurance Code of Practice, insurers are facing stricter timelines for claim decisions. Immediate notification remains your best protection against claim rejection and secondary mould growth.

Will my insurance pay for mould removal after a burst pipe?

Insurers generally pay for mould remediation if the growth is a direct result of a covered event, such as a burst pipe. They will likely cover the cleaning of affected surfaces and air purification if you acted quickly to mitigate the moisture. If the mould is deemed pre-existing or caused by neglect, the claim for those specific costs will be denied. Speed is the deciding factor here.

What is the “Escape of Liquid” clause in Australian insurance?

The “Escape of Liquid” clause covers the accidental release of water from fixed systems like internal plumbing, water tanks, or dishwashers. It’s a standard inclusion in most Australian home policies but focuses on the damage caused rather than the repair of the device itself. Understanding this clause is vital for navigating the water damage repair insurance process effectively. It ensures you are reimbursed for the restoration of your property.

Can I start cleaning up before the insurance adjuster arrives?

You’re legally required to take reasonable steps to prevent further loss before an adjuster arrives. This includes turning off the water, extracting standing pools, and moving furniture to dry areas. Ensure you capture detailed photos and videos of the “unfiltered” damage first. These records serve as your primary evidence once the professional restoration begins. Don’t discard any saturated items until they have been sighted or documented.

What happens if my water damage claim is denied?

If your claim is denied, you can request a formal review through your insurer’s Internal Dispute Resolution (IDR) team. If the outcome is still unsatisfactory, you have the right to lodge a dispute with the Australian Financial Complaints Authority (AFCA). Providing a restorer’s technical moisture report often helps overturn denials based on “gradual damage” assumptions. Technical evidence is your strongest tool during a dispute.

How much does professional water damage restoration cost in Sydney?

Restoration costs in Sydney are determined by the volume of water and the materials affected. Factors like the duration of the soak and the requirement for industrial dehumidification play a major role in the assessment. Your policy’s specific excess and coverage limits will dictate your out of pocket expenses. Always verify your “sum insured” to ensure it covers both structural repairs and contents replacement after a major event; additionally, to ensure your overall assets are managed effectively, you can learn more about Financial Mentors Wealth Management.

Is secondary mould growth covered by standard home insurance?

Secondary mould growth is covered if it occurs as a direct consequence of a sudden, insured water event. However, coverage is often contingent on you taking immediate action to dry the property. If you wait several weeks to report the leak, the insurer may argue the mould was a preventable “secondary loss” and refuse to pay. We provide the documentation necessary to prove the mould was unavoidable despite your best efforts.